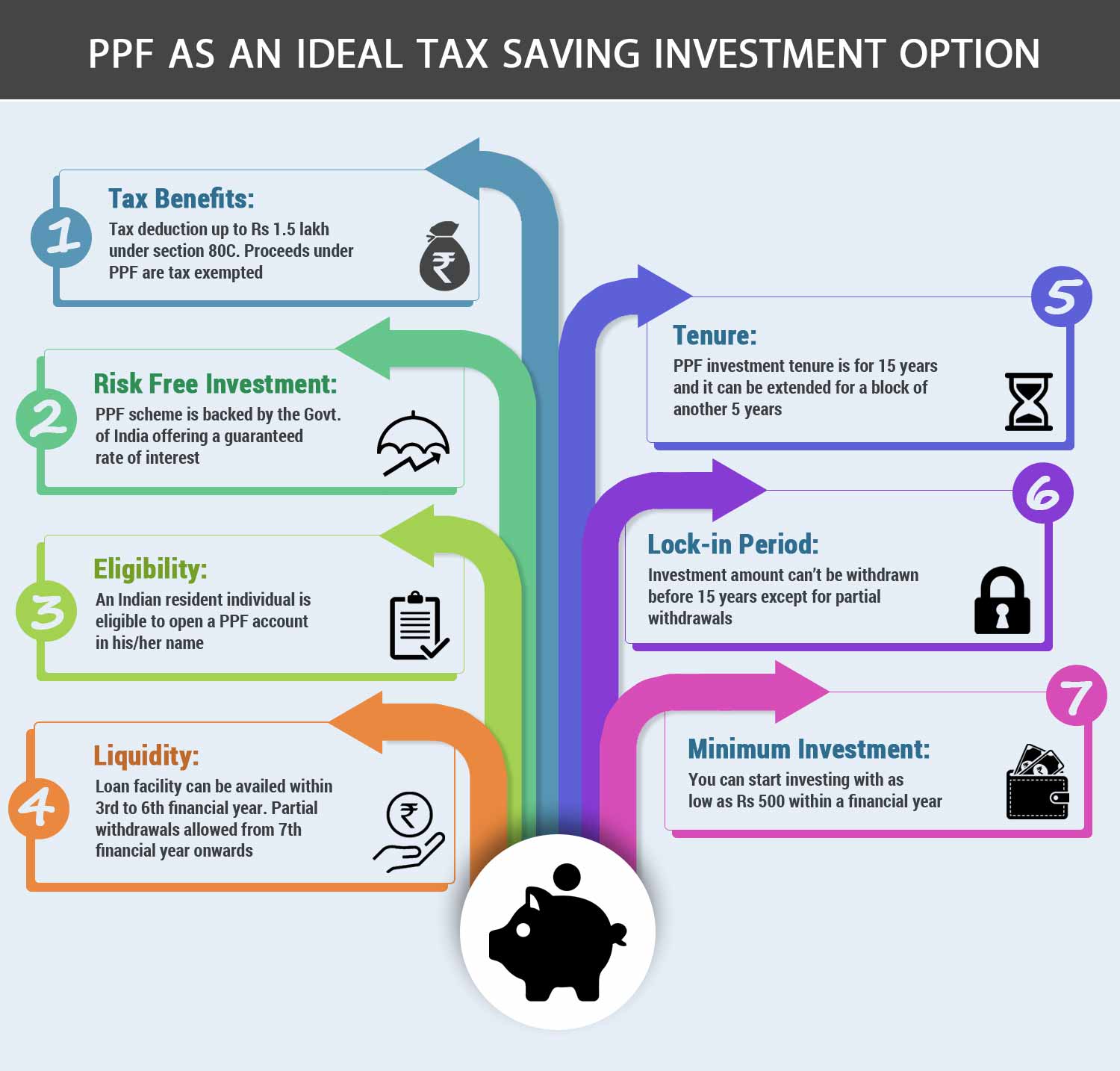

Tax Benefits under PPF

Apart from the key benefits available such as loan, partial withdrawal, and maturity benefit, investing in a PPF account also offers tax benefits.

Tax Deduction

Annual contributions made to a PPF account qualify for tax deduction under section 80C of the Income Tax Act, 1961. The tax deduction towards the money invested is capped up to Rs 1.5 lakhs for a financial year. You can also avail of tax deductions for contributions to PPF accounts of spouses and children. But the tax deduction availed cannot exceed 1.5 Lakhs if contributed to the PPF accounts of spouse and/or children.

Tax Exemption

Interest earned is exempted from income tax and maturity proceeds are also eligible for tax exemption. Any partial withdrawals made before the maturity date is also exempted from tax. Thus, you can avail of tax exemption for all the payouts received under a PPF account.

Key Things to Know About PPF Investment

There are some key aspects that you need to know before investing in the PPF scheme. Let’s go through some facts about the PPF, which will help you to make a well-informed investment decision.

Eligibility

An Indian resident individual is eligible to open a PPF account and start investing, however, opening a joint account is not allowed. A PPF account can be opened for a minor with a guardian (father, mother, or court-appointed guardian). A person is not allowed to open more than one account in his/her name. An account opened for a minor is considered separate. A grandfather or grandmother is not eligible to open an account on behalf of a grandchild, except in the case where a guardian has died.

Hindu Undivided Families, Non-resident individuals, or Body of Individuals are not allowed to invest in PPF. The account will be closed, in case an individual becomes an NRI. The interest paid from the date an individual becomes an NRI till the closure of the account shall be equal to the post office savings account interest rate, i.e., 4% per annum.

Account Opening

You can open a PPF account at all head post offices, other designated post offices, and at designated branches of the leading nationalized banks such as State Bank of India, Central Bank of India, Bank of India, Union Bank of India, Vijaya Bank, Allahabad Bank, Bank of Baroda, etc. Leading private banks such as ICICI Bank, HDFC Bank, Axis Bank, IDBI Bank, etc. have also started the facility to open a PPF account.

When you have decided to open a PPF account, you will need to provide the following documents.

- A duly-filled account opening form

- Two passport size photographs

- Identity proof (at the time of account opening, carry original identity proof for verification purposes)

- Address proof